Before you decide to invest into stock options there are some things you need to know. For example … how an option is priced. You should know more than this … but this is a good place to start. The things that impact the price of a stock option now and in the future are:

- the current stock price,

- the intrinsic value,

- the time to expiration or time value,

- volatility,

- interest rates and

- cash dividends paid.

You’ve all read or heard in the past that options can lose you a lot of money, and if done right they can make you a pile of money. Today’s article is going to deal with only two factors of a stock options price – the intrinsic value and the time value or extrinsic value.

Intrinsic Value

This is nothing more than the value per share of the underlying stock minus the strike price of the option. For Example:

- Assume Apple Computer (AAPL) currently is trading for $215.79 per share. If you purchased a call option with a strike price of $210 per share your option premium that you pay would include $5.79 of “Intrinsic Value.”

- However, if you were to purchase the $220 strike price call option and since “Intrinsic Value” can never be less that zero … your Intrinsic Value would be $0.00.

- Basically the “Intrinsic Value” is the amount by which the “Strike Price” is in the money.

So, with a call option the “Intrinsic Value” = Underlying Stock Price – Strike Price.

With a put option the “Intrinsic Value” = Put Strike Price – Underlying Stock Price.

Remember, when you buy a call option you are wanting the stock to increase in value and when you buy a put option you want the stock to go down in value. And now you know why some investors make money regardless of which way the market or stock moves.

This brings us to the next part of the price …

Time Value or Extrinsic Value

This is nothing more than the amount that is left over from the Option Premium when you deduct the Intrinsic Value. So, Time Value = Option Premium less Intrinsic Value. In an earlier article I wrote that “An option is like an Ice Cube. The day you buy it … it starts to melt.” I should have written, “An option is like an Ice Cube. The day you buy it the Time Value of the option premium starts to melt.” The only way the intrinsic value can melt away is if the stock price declines on a call option or increases on a put option.

It should be noted that time decay isn’t a linear function, meaning it doesn’t happen at a fixed rate. If an options contract has, say, 150 days until expiry, then the extrinsic value (aka Time Value) doesn’t diminish at the same rate for each of those 150 days. With 150 days to go until expiration, the rate will be quite slow, whereas with only 40 or 50 days to go the rate will be faster. Once there is less than one month to go, time decay will typically have much more impact on the extrinsic value. Basically, the closer the expiration date, the faster the rate of time decay.

The rate of time decay is measured by one of the options Greeks, Theta. The Theta value of an options contract theoretically defines the rate at which its price will decline on a daily basis. For example, the price of a contract with a Theta value of -0.03 would be expected to fall by approximately $0.03 each day.

You can find out the Theta value of most contracts by studying the appropriate options chain, but you should be aware that it’s only a theoretical value and not a guarantee of the rate of time decay. It can be useful to help with predicting the effect of time decay, but shouldn’t necessarily be relied upon. Because the rate accelerates as the expiration date gets closer to expiration, the Theta value will change accordingly.

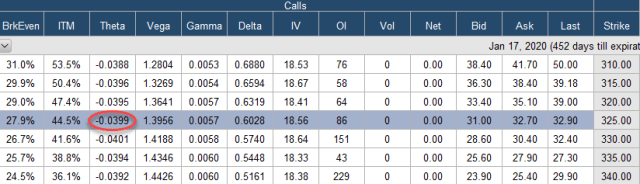

Here’s a call option chain for Lockheed Martin (LMT) 452 days from expiration:

Notice Theta of this option strike is -0.399 or a loss of about $0.04 cents per day.

Now look at this for the same strike just 39 days from expiration:

Theta has grown by almost 4X as the time decayed.

While Time Decay can negatively impact buyers of Call or Put options it can actually help sellers of Call or Put Options. However, this article is about buying and not selling.

When it comes to Time Decay … and to show it is not linear … you may want to visit the wonderful chart I found on the internet for an option with a 120 expiration time period.

You can see in this example (and it is only an example) that it could take 90 days for an out of the money options premium to decrease by 30% – but in the last 30 days the options premium (if it remains out of the money) could go to zero rather quickly.

Knowing this … why on earth would a person want to ever invest in options? It seems much safer to purchase the stock, doesn’t it? Not necessarily!

Let’s once again take a look at Apply Computer (AAPL) today as of this writing.

In the above table we see three different options on Apple Stock.

The first one with a strike price of $210 is considered an In The Money (ITM) option. Why? The strike price is $210 and the stock is selling for $215.79. With a premium of $30.45 (using the mid price between the Bid and Ask) the option would have an intrinsic value of $5.79 per share and a time value (or extrinsic value) of $24.66 per share.

The second would be considered an At The Money (ATM) option. It has a strike price of $215 with a stock price of $215.79 (can’t get much closer to being at the money than that). This would give the option an intrinsic value of $0.79 and a time value of $27.01 assuming an option premium paid of $27.80.

The third and final option represents an Out of the Money (OTM) option with a strike price of $220 while the stock is still at $215.79. This would bear a premium of $25.43 of which all of it would be considered time value since there is no intrinsic value.

Now when you look at the option symbol you will see a date represented by the first 6 numbers after AAPL. This is the expiration date and in this case it is stated backwards as 2020/01/17 – or January 17th, 2020. This means that 456 days from now the options will expire. If you were to purchase one and hold until expiration, if there is no intrinsic value – the option will expire worthless since the time value will go to zero. If there is intrinsic value (meaning the strike price is below the stock price) you will be assigned the stock at the strike price (again assuming you hold till expiration – and I don’t recommend doing that).

Remember, a call option gives you the right (not the obligation) to buy the stock at the strike price anytime before expiration on American Options. European Options are different – you only have the right on expiration date. If the option is out of the money at expiration it expires worthless. If the option is in the money at expiration and you do nothing you could be assigned the stock to replace the option. This means if you bought the $220 option on Apple and the stock is trading at $225 on the date the option expires, you would be assigned Apple at $220 (meaning you would have to come up with $22000 to purchase the stock). If you don’t have the $22,000 in your account you could purchase it and turn around and sell it for the market price of $225 per share or $22,500 in the case of 1 options contract.

While a call option gives the buyer of the call the right to purchase the stock at a set price, most option investors are not in the least bit interested in holding the stock so they do not want to own it. Most option buyers simply buy options to sell them later at a greater price … just like most stock buyers buy stock to sell it later at a higher price. The old adage of buy low and sell high is not only true for stocks and real estate but also for options.

Before going further – let’s examine the options symbol to understand what it means. I will only review the first one:

- AAPL200117C00210000

- AAPL represents the stock the option is on

- 200117 as stated before represents the expiration date of 01/17/2020

- “C” indicates it’s a Call Option. If it were a Put option it would include a “P” and not a “C”

- 00210 represents the strike price of $210 per share. If it were simply $21 per share it would be listed as 00021000. Notice there are three “0’s” in front of the 2 and three in back of the 1. As a number is added in the front a zero is dropped. As a number is added in the back a zero is dropped. If it were $210.50 per share (which it would not be on this high dollar stock) it would read 00210500

Now, if you purchase a call option and the price of the stock goes down … naturally the price of the option is going to go down. However, if you purchase a put option and the price of the stock goes down, the price of the put option will go up. Conversely if the stock price goes up the price of the put option will go down. Most people will purchase a call option believing the price of the stock is going to go up … and a put option believing the opposite will be true.

If you look at the chart of Apple for the past 10 years you can see that it has really been on a major trend upward. You should always check the charts before investing in Stock or Options and learn to “Make the Trend your Friend.” You would not want to purchase stock or a Call option if the trend is going down. However, you may consider selling the stock short (another article for later review) or buying a put if the trend is going down. In either case … “Make the Trend your Friend.”

I see no reason to think Apple will start a trend down in the near future … however we did see a trend down in 2013 and again in 2016 – though both of these were less than a year in length. Keep in mind, with the options I’ve picked we have 456 days (1.25 years) for the stock to trend. I’m pretty sure it will continue to trend up, though there are never any guarantees.

Let’s assume that the stock goes up by various percentage rates between now and say December 2019 (Notice I did not go all the way out to expiration and neither should you):

- If it goes up by 10% the stock will be worth $237.37

- If it goes up by 20% the stock will be worth $258.95, and

- If it goes up by 30% the stock will be worth $280.53.

This means that if I were to purchase 100 shares of stock at a cost of $215.79 per share today it could grow from $21,579 to …

- at 10% = $23,737

- at 20% = $25,895 and

- at 30% = $28,053.

This does not include any dividends that Apple may pay and they are currently paying $2.92 per share per year (or $292 on a 100 share lot), nor does it include commissions one might pay.

But when it is all said and done … what would the options do?

While I can’t give you an exact amount because I have no way of knowing how much time value would be left of the premiums (I would suspect maybe 10% or less by December 2019) – I can show you what the intrinsic value of the premiums would be based on these future projected stock values.

If the stock increases by 10%, the In the Money Option (ITM $210), the At the Money Option (ATM $215) and the Out of the Money Option (OTM $220) would be valued as follows (as it relates to intrinsic value only):

- Value of $210 Option = $237.37 – $210.00 = $27.37 or $2,737. Since you would have paid $30.45 … You would lose money.

- Value of $215 Option = $237.37 – $215 = $22.37 or $2,237. Since you would have paid $27.80 for these options … You would lose money.

- Value of $220 Option = $237.37 – $220 = $17.37 or $1,730. Since you would have paid $25.43 for these options … you would lose money.

- Of course you would do a little better than this since there would be some time value (though not much) remaining in December 2019.

As you can see, if the stock only goes up by 10% … you will not make any money by purchasing these options. You may do better buying the stock. People have asked in the past, “Jerry if my stock is going up in price … why isn’t my option making me money?” This could be the answer … it is just not going up enough or fast enough.

So … if you are thinking the stock could only go up by 10% over the next 1.25 years … you may want to stay away from this one. Remember, though, if the stock goes up 10% relatively quickly and there is still some “Time Value” left in the premium … you still could make some money on a 10% rise. You will see this later in a real example of my account.

What would happen at the 20% increase in value and the 30% increase in value? Would you do better owning the stock or the option. Take a look at the three tables below showing a 10% increase in stock price, a 20% increase in stock price and a 30% increase in stock price:

As you can see above, if Apple were to increase in value by 20% you could make between 53% and 61% on your options (depending on the one you purchased e.g ITM, ATM or OTM). If the stock were to increase by 30% your options could go up be 131% to 138% (again, depending on which one you purchased).

So, why did the 20% and 30% return do so well for options and the 10% return – even though the stock was up – lost money for the options? It could be that the options at the outset were over-priced since this is a heavily traded stock option.

The information in the next few paragraphs comes from Investopedia.com

There is a formula one could use to figure out if the options they were purchasing was over-priced or not. This is known as the Black-Scholes Formula and was developed in 1973 by three economist; Fisher Black, Myron Scholes and Robert Merton. This was introduced in their 1973 paper, “The Pricing of Options and Corporate Liabilities,” published in the Journal of Political Economy. Black passed away two years before Scholes and Merton were awarded the 1997 Nobel Prize in Economics for their work in finding a new method to determine the value of derivatives (the Nobel Prize is not given posthumously; however, the Nobel committee acknowledged Black’s role in the Black-Scholes model).

The Black-Scholes model makes certain assumptions:

- The option is European and can only be exercised at expiration.

- No dividends are paid out during the life of the option.

- Markets are efficient (i.e., market movements cannot be predicted).

- There are no transaction costs in buying the option.

- The risk-free rate and volatility of the underlying are known and constant.

- The returns on the underlying are normally distributed.

Note: While the original Black-Scholes model didn’t consider the effects of dividends paid during the life of the option, the model is frequently adapted to account for dividends by determining the ex-dividend date value of the underlying stock.

The formula, shown below, takes the following variables into consideration, if you are a mathematician you will have fun with this :

- current underlying price

- options strike price

- time until expiration, expressed as a percent of a year

- implied volatility

- risk free interest rates

Like I said, if your a mathematician you will have fun with that formula. As for me … I go with my “gut feeling” and a lot less research. My primary concern is the trend of the stock and the Time to Expiration. When buying options I always go long-term (6 months or more) and when selling them I always go short-term (2 months or less).

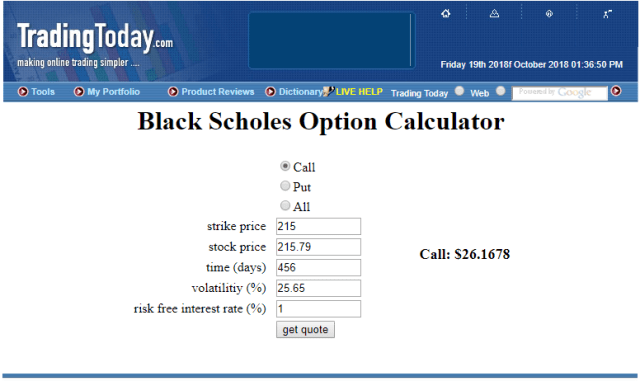

You can always go online and find a good Black-Scholes Calculator that you can use. You will need to know the Strike Price, the Stock Price, Days to Expiration, Volatility (can see this on the options chain) and the risk-free interest rate. Assuming a 1% risk free interest rate here’s what I came up with for the At The Money option on Apple.

As you can see they suggest a price of $26.17 for the ATM option vs. the $27.80 that showed on the options chain. So, while it was a little over-priced … it was not that much over-priced.

So, you are probably asking yourself, “Did Jerry buy options recently on Apple Computer and if so which strike price did he use?” The answer is No. I was simply using Apple as an example here. However, I did purchase options on Apple a few months ago and sold them recently.

Here’s the details of the purchase:

- On Aug 7, 2018 I purchased 2 contracts (=200 shares) for a total cost of $16.74 per share plus a commission of $6.28 on the two contracts. This gave me a total investment in these Apple Contracts of $3,354.28.

- The only thing I can tell you for sure is that on Aug 7, 2018 AAPL opened at $209.32 and closed at $207.11 – down a little over $2.00 for the day.

- I purchased the 06/21/2019 Calls with a strike price of $210 per share. Remember on Calls I like to go out long-term. While 10 months for a stock is short-term … it is considered long-term for options.

Now I told you I sold the options recently. Here’s a printout from my Schwab Account on this:

You can do the math …

- I closed the options (sold them) on October 11, 2018 just 65 days after purchasing them.

- On that date the AAPL stock opened at $214.52 and closed at 214.45.

- I sold my options for total proceeds of $4,505.91 and netted a profit after commissions of $1,151.63.

- This represents a total % Return on Investment (ROI) of 34.33% in 65 days while the stock itself was only up $5.13 or 2.45% in the same period of time.

- If one would simply annualize my return over 365 days you’d find you come up with a return of 192.78% (of course assuming I could replicate the same return every 65 days for a year).

So, how is it that the stock in this example only went up 2.45% and I made 34% on the option while showing an increase in value of 10% above on Apple and losing money in the options. Remember … I was not calculating in time value only Intrinsic Value since time value would have been so low. In this example because I sold early there was both intrinsic value and time value remaining. I paid $16.77 per share (including commissions) and had intrinsic value of 0.00 – it was all time value. I sold the contracts when there was $4.52 of intrinsic value plus a lot of time value remaining.

The Dogs of the Dow …

I have had similar returns by investing in options on the Dogs of the Dow! What are the Dogs of the Dow?

Much of the information in the next few paragraphs from from Investopedia.com

The Dogs of the Dow is an investment strategy popularized by Michael B. O’Higgins in 1991, which proposes that an investor annually select for investment the ten Dow Jones Industrial Average (DJIA) stocks whose dividend is the highest fraction of their price.

Proponents of the Dogs of the Dow strategy argue that blue-chip companies do not alter their dividend to reflect trading conditions and, therefore, the dividend is a measure of the average worth of the company; the stock price, in contrast, fluctuates through the business cycle. This should mean that companies with a high yield, with a high dividend relative to stock price, are near the bottom of their business cycle and are likely to see their stock price increase faster than low-yield companies.

Under this model, an investor annually reinvesting in high-yield companies should out-perform the overall market. The logic behind this is that a high-dividend yield suggests both that the stock is oversold and that management believes in its company’s prospects and is willing to back that up by paying out a relatively high dividend. Investors are thereby hoping to benefit from both above-average stock-price gains as well as a relatively high quarterly dividend. Of course, several assumptions are made in this argument.

The first assumption is that the dividend price reflects the company size rather than the company business model. The second is that companies have a natural, repeating cycle in which good performances are predicted by bad ones. Due to the nature of the concept, the Dogs may come from a small number of sectors. For example, the ten stocks that belonged to the 2015 Dogs of the Dow list came from only six sectors, including industrials, energy, and healthcare, in contrast to the S&P 500 Index which covers eleven sectors.

Since the Dogs of the Dow contains 10 stocks, some people with smaller portfolios prefer to invest in the Small Dogs of the Dow – which is the lowest priced five of the ten Dogs. I call these the Puppies of the Dow. In some of my portfolios I may hold the stock outright and sell call options against them. This is known as a Buy-write strategy (I will do an article about this later) or selling Covered Calls. In my Options ONLY portfolio I am known to buy options on these puppies from time to time (usually about 4 times per year or quarterly).

All of the options have an exercise date of one year or longer because these bigger companies allow options to go out longer. These are called LEAPs (Long Term Equity Anticipation Securities) which are options of longer terms than normal options.

For this article I looked at the DJIA and chose the top ten stocks with the highest dividend yield over the past 12 months. I then decided to look at one option at the money and one option with a strike price just out of the money. The table below shows what I came up with at the time:

Since these are listed by stock price (lowest to highest) the five Puppies will be at the top and the five Big Dogs will be at the bottom.

Now, had I purchased one contract of each of these At the Money and one contract of each of these out of the money (controlling 200 shares of each stock) I would have made an investment of $14,511 on the day I put this together. If, on the other hand I simply purchase 200 shares of each of the stocks at the market price, I would have had to invest $175,066. Folks, this is “Leverage.” In fact I am controlling $12.06 worth of stock for only a little more than 8 cents. Now some will tell you that LEVERAGE involves RISK.

If all the stock declined by 10% I would lose $17,507 approximately. If all the options expire worthless, I would lose only $14,511. You tell me … Where’s the biggest risk in terms of potential dollars lost?

But, what if I did purchase all the options and all the stocks listed went up by 10%, 20% or 30% between now and say December 2019 (these are also January 17, 2020 expiration dates) based on the Intrinsic Value alone? Take a look at the following three tables:

At 10% Stock Growth

At 10% stock growth I would make $17,506.60 on a stock portfolio and only $711.60 on the options portfolio (based on intrinsic value alone). Some of the options could have lost me as much as 44% while others did in fact out-perform the stock.

At 20% Stock Growth

Here while the stock portfolio returned an overall return of $35,013.20 or 20% … the options portfolio did better based on a percentage return of 125.55%. I really have no problem investing $14,511 and getting back $32,729 a year or so later.

At 30% Stock Growth

This, of course, was best overall. A 30% gain on the stock portfolio was dwarfed by a 246% gain on the options portfolio.

So, what did I actually buy after all this? My goal was to invest about $10,000 into options contracts and to make sure that the most I could lose on any one investment was no more than 2% of my total options portfolio value (about $50,000).

This means the most I should invest in any one holding would be $50,000 X .02 = $1,000. However, since like stocks, you cannot purchase fractional contract values … some of the investments would be a little more than $1,000 and some would be a little less than $1,000. If you look in the cost basis column (5th from the right) in the snapshot below you will see that I actually was able to invest $9,899.32 on 10/17/2018.

Below I have put in a copy of what my Schwab Account looks like today (10/18/2018):

After the first day you can see that my investments had gained $2,198.00 or 28.07%. Due to a very positive earnings report … Proctor & Gamble was up 84.56% with my worst performers being Cisco at 3.15% and 3.23% – which really is not bad after one day.

Now I am not telling you this to “Brag on my smartness” because I am really not that smart, though I have been called a “Smart Ass” from time to time during my life. I actually came upon this investment scheme purely by accident.

I was reading an article about how the Dogs of the Dow historically have beat the Dow Jones Industrial Average year after year … and how the Small Dogs of the Dow (the puppies as I call them) have done even better on a pure Return on Investment than all the Dogs.

You can go to www.dogsofthedow.com and read more detail about investing in these companies stocks each year. While I was reading articles about this investment program I got to thinking that, “if the stock did this well … how well would the options do.” I started this program in 2016 and turned $30,000 of investment dollars into about $85,000 of capital within a year. I was able to purchase my 2017 Silverado with those gains and pay cash for it. In 2017, I did not do as well … but still managed a gain of greater than 100% for the year.

The year 2018 has been a little tougher … but still I was able to generate profits of 53.49% in a period of an average of 281 holding days, as represented by the table below:

Yes, it is true, I lost as much as 83% on some holdings (P&G for one) … but remember the question I always ask myself … “Can I afford to lose $X Amount if this investment goes all the way to zero.” I can comfortably answer “YES” because although I am not that smart I do know that I will not lose on all of them … and the ones I gain on should outweigh those that I lose on. In this illustration I lost on 10 of the investments … but made money – GOOD MONEY – on 12 of them. In a terribly tough market environment that is still a win ration of 55%. Keep in mind I am only showing my Call Options on the Dow Puppies since that is the purpose of this article. Until I gain more personal experience in Put Options … I will leave that for a future article.

Moral of this Story:

My purpose for writing this is not to brag – as I said previously. Nor is it to get you to not follow the advice of your financial advisor since he or she knows your situation much better than I do. However, realistically thinking, your financial advisor will not always be there to provide good advice. He or she could retire or even die before you do. You need to have some knowledge of how investments work and that was the real purpose of this article.

I am not suggesting that you stop buying stocks, Exchange Traded Funds or Mutual funds altogether and strictly invest in stock options. I think you need to consider them all, and it is easy to do. Warren Buffett, one of the wisest investors in the world says, “I never attempt to make money on the stock market. I buy on the assumption that they could close the market the next day and not reopen it for five years.” And that is very true when it comes to investing in stocks. However, to my knowledge there are not any options that will go out for a period of five years. The longest I’ve seen is 18 months to 2 years. I do think you should invest in options on companies you would buy and hold for five years or more. You can do so at a fraction of the cost. Warren Buffett also says, “Cost is what you pay and value is what you get.” Buying options can provide you that tremendous value.

So next time your financial advisor tells you to purchase 100 shares of Lockheed Martin (LMT), as an example, an investment that would cost you $326.55 (or $32,655 for 100 shares) – and you know you would not be buying it if you and your financial advisor did not believe it was going to go higher in the next one year (know one really looks out five years when it comes to investing their money – though they may hold it for five years or more, but they want it going up immediately) – so consider this:

- Consider investing a fraction of the money ($32,655) into some January 2020 options and the remainder into the stock.

- You could buy the January 2020 $325 strike for $32.90 today, or

- You could buy the January 2020 $330 strike for $32.40 today.

- This would be a total cost of $3,240 to $3,290 for the option which would still leave you $29,365 to $29,415 to put into the stock.

- This would still allow you to purchase at least 90 shares of LMT today. Reinvest your dividends (Currently at $8.80 per share) and you’d be able to purchase more shares each year ($792 received after the first year) so that within the five year time frame you would have 100 shares and you and your financial advisor would be happy.

- And, during that five years … you could use options at least 3 times.

That’s it for today. If you would like to get in on this investment scheme and are not sure how to go about it … please write or call me. The first step is to read as much as you can about options and how they work and you can do that right here https://www.theocc.com/education/ or right here https://www.investopedia.com/university/options/option3.asp… but I believe you will really never learn them until you put some money on the table and convert the learning into earning.

Have a great year, write an Options Investment Plan and follow the plan. You too can become a Wave-maker!

Jerry Nix