By: Jerry Nix | Freewavemaker, LLC Date Published: October 30, 2023

Stupid Investors:

I hear about the difference between what a person can earn by putting money in the bank as compared to investing in Guaranteed Government Issued securities and it really amazes me that “stupid” investors buy into the garbage the government in America is selling.

Don’t they know where the government has to get the money to pay interest on their debt? Don’t they understand that when they invest in government securities, they are not buying stock in America but rather helping America go broke?

The purpose of this article is to give you the facts in hopes that you will direct your money elsewhere:

FACT 1: Bank Returns Now

Certainly, you don’t want to consider putting a lot of money in the bank with the piddly return’s bankers are paying. Inflation has driven interest rates higher but you can’t tell it looking at what Mr. Banker is willing to pay you park large sums of money there.

The interest rates being paid by banks on various deposits vary depending on the type of account and the term of the deposit. As of October 30, 2023, the following are some average interest rates being paid by banks on various deposits:

- Savings accounts: 0.46%

- Interest checking accounts: 0.07%

- Money market accounts: 0.65%

- 1-month certificates of deposit (CDs): 0.22%

- 3-month CDs: 0.34%

- 6-month CDs: 0.51%

- 12-month CDs: 0.87%

- 24-month CDs: 1.23%

- 36-month CDs: 1.55%

- 5-year CDs: 2.01%

It is important to note that these are just average interest rates. Some banks may offer higher or lower interest rates depending on their competitive landscape and other factors.

Now let’s look at this … take the best return from above … a 5-year CD paying 2.01%. What is the banker going to do with your money? He will loan it to someone at a rate of 7% per year – and in effect – you are paying almost 5% per year to park your money there. After taxes and inflation, you are into negative return territory.

When I worked in the financial services industry, I’d catch grief from clients because they would invest money into a mutual fund and would be charged a 5% sales load … one time … and those same people were okay with the bank charging them 5% per year, every year, their money is there. It just does not make much sense to keep a lot of money in the bank with the piddly amount the banks are willing to pay you.

The banks do not guarantee your money or a return … but they do insure it up to $250,000 per account through the FDIC.

FACT 2: The FDIC Insurance not as secure as you think …

According to the FDIC’s website, as of September 30, 2023, the FDIC has $131.9 billion in reserves, which is enough to cover 1.1% of all insured deposits.

This means that for every $1,000 that is insured by the FDIC, the FDIC has $11.19 in reserves.

The FDIC’s reserves are made up of a variety of assets, including cash, Treasury securities, and loans to banks. The FDIC uses its reserves to protect depositors in the event that a bank fails. And it may if one or two banks fail … but what happens if we have a high rate of bank failures like we had savings and loans failures in the early 1980s?

The FDIC also has a line of credit with the US Treasury Department, which it can use to access additional funds if needed.

But ask yourself … what would happen if there were a major run on banks like we had during the great depression of 1929-1933. What would literally happen to the FDIC?

Well, what about U. S. Treasury Securities … they are said to be guaranteed (if you hold them till maturity)?

FACT 3: U. S. Treasuries hurts the country more than they help it…

Let’s first take a look at the returns being offered today on some of these US Treasury Securities.

The interest rates of current issues of government bonds and notes vary depending on the maturity of the security. As of October 30, 2023, the following are the interest rates of some recently issued Treasury securities:

- 3-month Treasury bill: 3.375%

- 6-month Treasury bill: 3.675%

- 1-year Treasury bill: 3.975%

- 2-year Treasury note: 4.275%

- 5-year Treasury note: 4.575%

- 10-year Treasury note: 4.875%

- 20-year Treasury bond: 5.175%

- 30-year Treasury bond: 5.375%

Now as you can see … it does not make much sense to tie money up in a CD for 5 years for 2.01% when you can tie it up in these kinds of securities between 3 months and 5 years for a return of 3.375% to 4.575% – does it? All of these returns are greater than a 5 year CD with a lot less of a holding period.

Keep in mind though that what you are seeing here is the yield (or coupon rate) at issue based on the face value of the instrument. For example … if it were possible to invest $10,000 into a 2-year Treasury Note and 4.275% … you would earn $427.50 per year for two years and at the end of the two years you could get your $10,000 back.

But what happens in the meantime. While the 4.275% is continued to be paid … if interest rates go up and you need to cash in the Treasury Bill you are not going to get $10,000 back because as interest rates rise the value of these decline. If, on the other hand interest rates decline and you need to cash in this Treasury Bill you will likely get more than $10,000 back because as interest rates decline the value of the investment goes up.

It works like a teeter-totter …

So far this does not seem bad. However, ask yourself … Just where does the government get the money to pay you the interest on these so-called securities?

Remember the Federal Government does not make or sell anything so it cannot create income from honest work.

The government gets the money to pay interest on its bonds and notes from a variety of sources, including:

- Tax revenue: The government’s primary source of revenue is taxes, which it collects from individuals and businesses. This revenue is used to fund all of the government’s operations, including paying interest on debt. The more debt, the higher taxes will have to go.

- Borrowing more money: The government can also borrow more money to pay interest on existing debt. This is typically done by issuing new bonds or notes. The more debt the more the government may have to borrow which leads only to deeper debt.

- Selling assets: The government can also sell assets, such as land or buildings, to raise money to pay interest on debt. And when you buy government assets (Army surplus as an example – you get it for pennies on the dollar … not the fair value of the property). Very STUPID government.

In addition to the above sources, the government can also print money to pay interest on debt. However, this is generally considered to be a last resort (though lately it is a resort that is used more often than not), as it can lead to inflation (and this could be a major reason we have inflation that can’t be brought under control today). The more we print, the higher the debt and the more the debt the higher the inflation rate.

The government’s ability to pay interest on its debt is important because it helps to maintain the government’s creditworthiness. If the government defaults on its debt, it will be difficult to borrow money in the future. This can lead to higher interest rates and make it more difficult for the government to finance its operations.

According to the US Department of the Treasury, China owns $859.4 billion in US debt as of October 30, 2023. This makes China the second-largest foreign holder of US debt, after Japan. Do we want to continue to be indebted to China and Japan?

In my opinion, the more we average American’s or rich American’s buy into the governments need to sell securities to us for nice interest rate returns … the more we are enabling them to possibly run our deficit so high that the country could eventually have to default on loans to American Citizens, Investors and foreign countries or end up forcing us to live with the inflation rates of these countries …

According to the World Economic Outlook (October 2023) by the International Monetary Fund (IMF), the highest inflation rate in the world today is in Venezuela, at 360%. This is followed by Zimbabwe at 172%, Argentina at 113%, Sudan at 71.6%, and Turkey at 47.8%.

Then, tell me how bad you think 7% inflation really is.

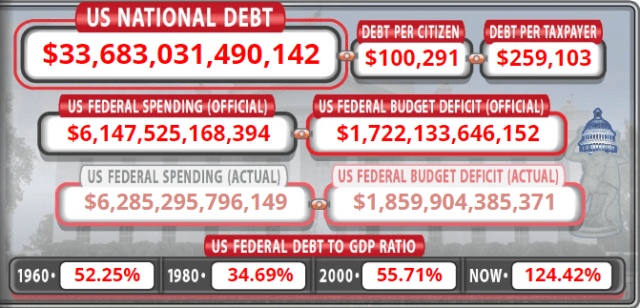

It has taken me about an hour, so far, to write this article. In that amount of time our deficit in this country has gone from $33,687,031,490,142 to …

That is an increase of $4.265 trillion to the national debt per hour.

Yes, currently the US adds on average $4.265 trillion to the national debt per hour in 2023. This is calculated by taking the total national debt of $30.98 trillion as of October 30, 2023, and dividing it by the number of hours in a year (8,760).

It is important to note that this is just an average. The actual amount of debt that the US adds each hour can vary depending on a number of factors, such as the government’s spending and revenue levels.

For example, during the COVID-19 pandemic, the US government ran a large budget deficit as it spent heavily on stimulus measures to help the economy. This led to a significant increase in the national debt.

In the long term, it is important to reduce the national debt to ensure the fiscal sustainability of the United States. This can be done by reducing government spending, increasing government revenue, or a combination of both. One sure fired way to decreases government spending is for Stupid Investors to quit buying into Government Securities as individuals, corporations and foreign countries. Of course, we also need to clean house when it comes to congress. Put people in charge that understands money and the proper use of it.

So, what can a person do that is interested in high earnings and potential growth of capital?

If nothing else consider keeping adequate cash reserves in the bank and then invest for the longer term in dividend producing stocks that have a track record of growth of price and growth of dividends. Some of these companies would be the oldest companies in America. Here’s one name that comes to mind … Johnson & Johnson (JNJ)

This is not an investment recommendation … consult with your investment advisor for such recommendations. It is meant for educational purposes only.

Johnson & Johnson (JNJ) was founded in 1886, making it one of the oldest and most established healthcare companies in the world. Over the years, JNJ has grown into a global leader in pharmaceuticals, consumer health, and medical devices.

JNJ’s performance over time has been impressive. The company has generated positive earnings every year for over 90 years. In addition, JNJ has a long history of dividend growth. The company has increased its dividend for 61 consecutive years, making it a member of the Dividend Aristocrats.

Here is a summary of JNJ’s performance and dividend growth since 1995:

The green line is the weekly price action which has gone from $17.19 per share on 06/16/1995 to $146.48 per share on 10/23/2023 – an increase of 752.123% in the past 24 years 3 months (an increase of 9.23% per year compounding monthly). The blue area represents the increasing dividend annually that has gone from $0.33 per share to $4.76 per share – an increase of 1,342.42% over 24 years 3 months (an increase of 11.63% per year compounded monthly).

So, while this investment – or any stock – may not be guaranteed to return you a gain … long-term I think most investors would be much happier holding something like this than holding an investment that only hurts America worse.

But then, my friends, loaded with the facts … you will have to decide what is best for you in light of your goals, ambitions and risk tolerance.

So, decide … and have a good day. Remember though … “You can’t row the boat without “making waves” and if you are not rowing the boat, you are likely only drifting where the currents take you” ~ Jerry Nix | Freewavemaker, LLC